RU

RU

CN

CN

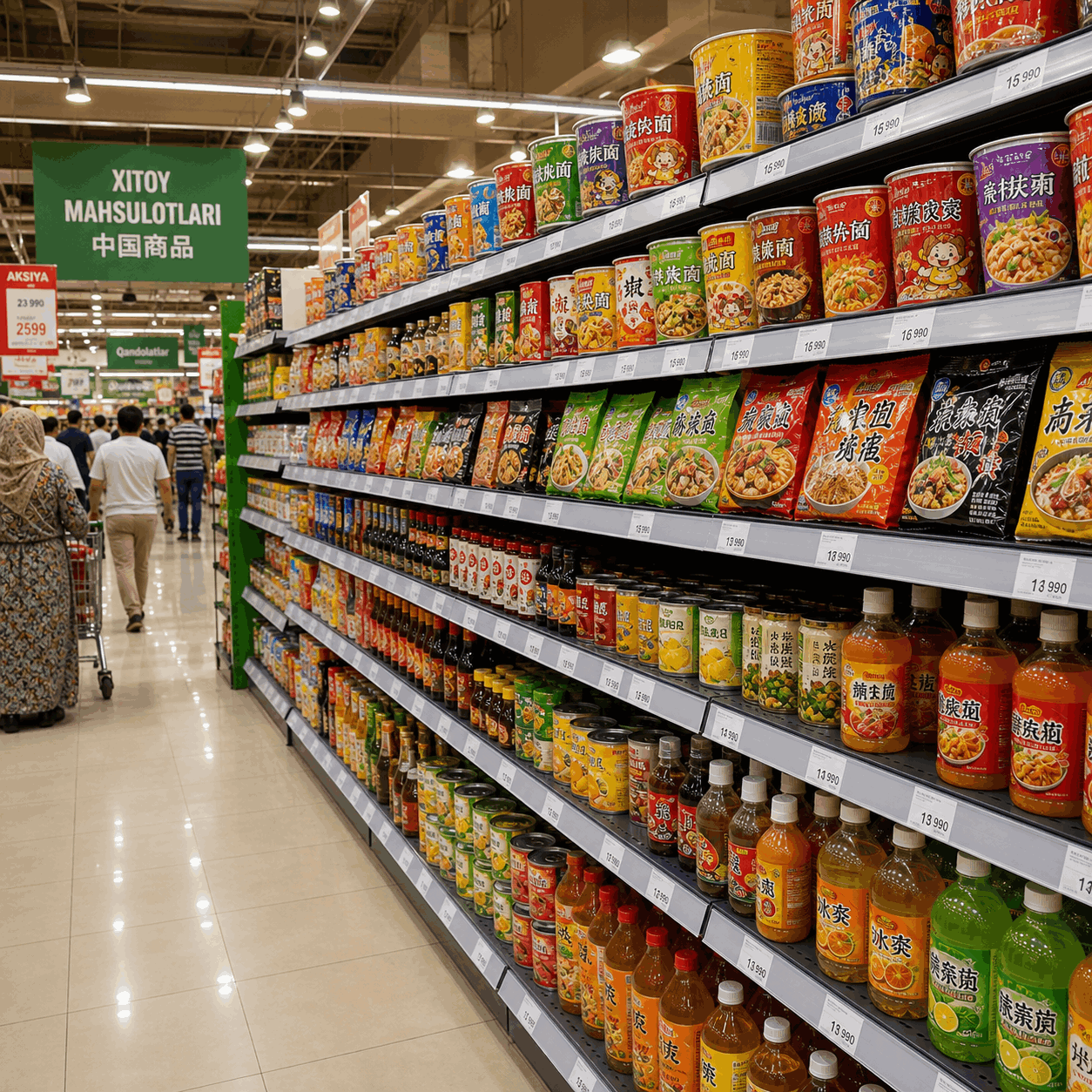

China expands its presence on Uzbekistan food shelves

In 2025–2026, Uzbekistan continues to increase its imports, while China is consolidating its status as the country’s largest foreign trade partner. Against this backdrop, food supplies from the People’s Republic of China are steadily expanding, although they still remain smaller in scale compared to Chinese exports of machinery, equipment, electronics and industrial goods.

For the FMCG and food retail market, this is an important signal: the Chinese direction is no longer perceived exclusively as a source of non-food assortment and is increasingly entering Uzbekistan’s food matrix – primarily in the segments of ready-to-eat products, snacks, beverages, sauces, processed fruit and vegetables and food ingredients. Combined with the price flexibility of Chinese suppliers, the expansion of logistics corridors and the continued interest of Uzbek retailers in affordable imports, this forms a stable trend towards further strengthening of China’s position in the country’s food imports.

China strengthens its position in Uzbekistan’s foreign trade

According to official statistics, in January 2026 China accounted for about 35 percent of Uzbekistan’s imports and ranked first among the country’s foreign trade partners. In 2025, trade turnover between China and Uzbekistan reached around 16.1 billion US dollars, having increased by nearly 18 percent compared to the previous year. At the same time, total imports of Uzbekistan in 2025 grew to approximately 47.4 billion US dollars, which is 18.5 percent higher than in 2024.

This means that any expansion of Chinese export offerings automatically affects the country’s food market as well. Although official statistics often group goods into broader categories rather than providing open, detailed breakdowns for each food segment imported from China, the very logic of the trade structure shows that the higher the overall volume of imports from China, the more noticeable becomes the presence of Chinese food products, especially in categories with high turnover and strong price competition.

Food imports from China are growing along with Uzbekistan’s overall food imports

In 2025, Uzbekistan’s total food imports are estimated at about 4.5 billion US dollars, which is 23.5 percent higher than in the previous year. In April 2026 alone, food imports reached 564.4 million US dollars, showing a 43.4 percent year-on-year increase. This confirms that the country’s food imports are in an acceleration phase, which means that the window of opportunity for Chinese suppliers is also expanding.

Within this structure, China is not yet the dominant supplier across all food categories. However, it is strengthening its position in those areas where price, manufacturing scale, flexible packaging and the ability to quickly adapt the assortment to the needs of distributors and retail chains are particularly important. First and foremost, this refers to ready-to-eat mass-market products, semi-finished foods, snack categories, beverages, sauces, confectionery, frozen and processed fruit and vegetables, as well as ingredients for the local food industry.

Most promising categories

The most significant potential for Chinese food imports to Uzbekistan is concentrated in several segments.

- Snacks and ready-to-eat products: chips, dry snacks, seaweed snacks, biscuits, cookies,

- Asian flavour lines, products targeting younger consumers and convenience retail.

- Beverages: tea-based drinks, functional beverages, ready-to-drink formats, juice-based drinks,

- Asian-flavoured beverages and low-priced mass-market products for modern trade.

- Sauces, seasonings and Asian cuisine products: soy sauce, spicy sauces, instant noodles, broth bases, soup bases and culinary ingredients for both HoReCa and retail.

- Processed fruit and vegetables: canned, dried and frozen fruit and vegetables that fit well into the segment of affordable imports and are supported by resilient logistics.

Ingredients for processing: food additives, flavourings, components for beverages and confectionery that are in demand among local manufacturers. An important point is that Uzbekistan remains a market with a fast-changing consumer structure. Urbanisation, the growth of modern trade and the expansion of assortments in retail chains create demand not only for basic products but also for low-priced novelties that allow retailers to refresh their shelves without a sharp increase in wholesale purchase prices.

What supports demand for Chinese imports

One of the key drivers is state policy aimed at reducing the cost of certain imported categories. Until the end of 2025, Uzbekistan maintained zero customs duties on 36 categories of food and consumer goods. The list of preferential items included meat, fish, dairy products, vegetables, fruit, flour, grain, confectionery, sauces and a range of ready-made food products, which created a favourable environment for external suppliers, including Chinese exporters.

The second factor is the development of transport connectivity between China and Central Asia. New and expanded corridors within the cooperation framework between China and the countries of the region reduce delivery times and transaction costs, which is especially important for FMCG categories with high delivery frequency and tough price competition.

The third factor is Uzbekistan’s domestic consumer market, which in 2025–2026 remains on a growth trajectory and becomes increasingly attractive for international suppliers of mass-market products. While price sensitivity of the population remains high, local retailers are simultaneously looking for new formats, flavours and categories that can differentiate the shelf and attract younger audiences.

Constraints and risks

Despite the positive dynamics, food imports from China to Uzbekistan face a number of constraints. First, official statistics do not always allow quick, open access to full, detailed breakdowns specifically for food categories imported from the People’s Republic of China without relying on specialised customs databases. This complicates precise assessment of China’s share in individual categories and requires additional verification by HS codes.

Second, requirements for food safety and quality remain strict. When importing controlled products into Uzbekistan, authorities apply documentary, physical and laboratory checks, which raises the bar for certification, labelling and the stability of suppliers. For Chinese manufacturers, this means the need to localise their offerings more deeply for the Central Asian market, including adapting recipes, packaging and, in some cases, obtaining halal certification and tailoring branding to local norms.

Third, competition is intensifying. In food imports, suppliers from Russia, Kazakhstan and other countries hold strong positions, especially in basic categories where logistics are simpler or traditional trade ties are stronger. As a result, Chinese companies are most competitive in those segments where they can offer not only a low price, but also new product formats, innovative assortment or flexible private label solutions.

Implications for retail and distribution

For retail chains, distributors and importers in Uzbekistan, the Chinese direction is becoming increasingly attractive as a source of low-cost and quickly scalable food SKUs. This looks particularly promising in the niches of snacks, beverages, sauces, Asian cuisine, functional products and in the segment of contract manufacturing for private labels.

From a strategic perspective, the market is entering a phase where Chinese food suppliers can compete not only on price but also on speed of product launch, packaging and assortment customisation for local retail. For modern trade in Uzbekistan, this opens opportunities to expand the offer without sharply increasing final prices for consumers, while local distributors can build more profitable portfolios in impulse demand categories.

For the market of Uzbekistan, Chinese food products today are no longer an occasional import, but an emerging direction with clear commercial logic. As modern trade, demand for ready-to-eat solutions and private label strategies develop, the role of the People’s Republic of China in food imports will strengthen primarily in high-rotation, flexible and price-sensitive categories. The main conclusion for retail and suppliers is to look at China not only as a source of non-food assortment but also as a full-fledged platform for developing the next generation of food categories – from snacks and beverages to ingredients and Asian cuisine products. Over the next 12–24 months, the speed of assortment adaptation to local demand will largely determine who can secure the best positions in this direction.